March 13, 2023

BIOINVEST NEWS: Sorting Through The Rubble – Buy The Best-In-Class Compounds (CLDX, MDGL)

Biotechs were under pressure this week as the sudden failure of SVB and drug pricing concerns delivered a double whammy in a continued rising rate environment. In our view, while all biotech stocks are being sold indiscriminately, we believe the economic fallout will eventually lead to the Fed slowing down. Moreover, we strongly believe that neither (the bank failure nor the Biden budget proposals) will lead to any material negatives for the sector. Overall biotech fundamentals remain intact. And although the financing environment will remain rather difficult, the majority of MTSL companies with attractive compounds and data are not only doing well fundamentally, but the vast majority are well capitalized, too.

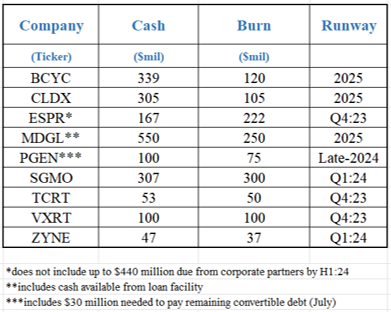

In light of the banking weakness on Wall Street and particularly Silicon Valley Bank’s collapse, we thought it is important to review the balance sheets, cash positions and burn rates for the development stage MTSL Universe. The list below does not include our late-stage recommendations that are extremely well financed and/or profitable including ACAD, ALKS, BMRN, IONS, INCY, and PCRX. Out of our total MTSL Universe, roughly 80% are in great shape financially:

Of the list above, BCYC, CLDX and MDGL are in excellent shape financially (as well as fundamentally – with all three delivering strong clinical results for their respective lead compounds during the past three months). TCRT, VXRT have under a year’s cash and will need to deliver value adding catalysts to avoid dilution at currently depressed valuations. In our view, both companies have the potential to deliver the good data that will allow them to raise capital at better terms that their current stock prices suggest. SGMO recently filed an 8K that they were in discussion to raise with institutional investors but shut it down believing they have enough coming in with partners and other corporate deals coming near term. ESPR should be able manage their cash needs as the CLEAR Outcomes data will trigger over $400 million in partner milestones which they can monetize early if absolutely needed. In addition, the recent good showing at the ACC will also lead to an immediate solid bump in Nexletol sales. Finally, one reason PGEN bounced on its recently quarterly release is that it announced it has paid off a vast majority of its $200 million convertible debt (~90%) that is due in July.

SVB’s main clients are tech and private biotech companies and its collapse caused a selloff in the biotech sector. Private biotechs that rely on VC money will have to find alternatives to SVB but their fate does not affect the public biotechs. Most of the money will get paid back by the Feds minimizing the damage, however private biotechs just lost their bank of choice which hurts them short term, but has minimal impact on the public biotech sector. We think the risks to the biotech industry are minimal overall as there are numerous banks ready to step in and provide similar fundraising and lending. SGMO was mentioned in a recent article that they are exposed to SVB but with over $300 million in cash we believe their cash needs are more than adequate. (In fact, we believe they will form a partnership this year bringing in further non-dilutive cash.)

President Biden’s budget proposal came with some pretty harsh recommendations for drug price reform that go far in excess of the IRA of 2022. Industry will fight this tooth and nail and the proposal has little to no chance of passing and most likely represents a “political bone” to progressives in the party. In our view, neither SVB’s collapse or Biden’s most recent drug pricing constraints are material negatives for the sector and we expect a near term bounce as the biotech selloff is overdone.

We strongly recommend taking advantage of the dislocation in our best fundamental and financially sound mid-stage stocks above, in particular Celldex (CLDX) and Madrigal (MDGL). These two have best-in-class compounds in multiple blockbuster markets, strong cash positions and catalysts in 2023. In these markets, we also believe they are two ripe takeover candidates as the Big Pharma/Bios are shopping to bolster pipelines; hence, we believe there is a good chance that – like most best-in-class compounds with de-risked clinical data – historically they will one day be bought at significant premiums.